Numbers Don’t Back Mayor Stewart’s Claim That State Budget Caused City’s Negative Credit Rating

By John McNamara

Contributing Columnist

Mayor Erin Stewart has blamed this year’s state budget crisis for the city’s negative credit rating in response to a November 2nd report of an “escalating” debt and her administration’s own budget that shows interest payments will cost taxpayers tens of millions of dollars over the next four years.

“We were downgraded by Moody’s along with many other cities and towns across Connecticut as a result of the state budget crisis,” the two-term Republican told the New Britain Herald.

“We were downgraded by Moody’s along with many other cities and towns across Connecticut as a result of the state budget crisis,” the two-term Republican told the New Britain Herald.

Democratic Mayoral Nominee Merrill Gay, citing double-digit tax increases and a debt load rising to “$75 million”, said Ms. Stewart is mismanaging the city’s finances. “Mayor Stewart’s poor financial planning will cost New Britain taxpayers,” Gay said. “New Britain needs real economic development without increasing the debt despite two tax increases.”

The state Legislature, dealing with deficits caused mainly by unfunded pension liabilities, finally adopted a biennial state budget at the end of October after a four-month stalemate.

The state Legislature, dealing with deficits caused mainly by unfunded pension liabilities, finally adopted a biennial state budget at the end of October after a four-month stalemate.

While the protracted debate in Hartford created short-term uncertainty for cities and towns, New Britain will maintain state aid amounts it gets as an economically distressed community. In the current fiscal year that ends June 30, 2018, state aid will be a projected $101 million to pay for schools and government — the same as it received last year. In 2019 the city will be cut by $191,000 from 2017.

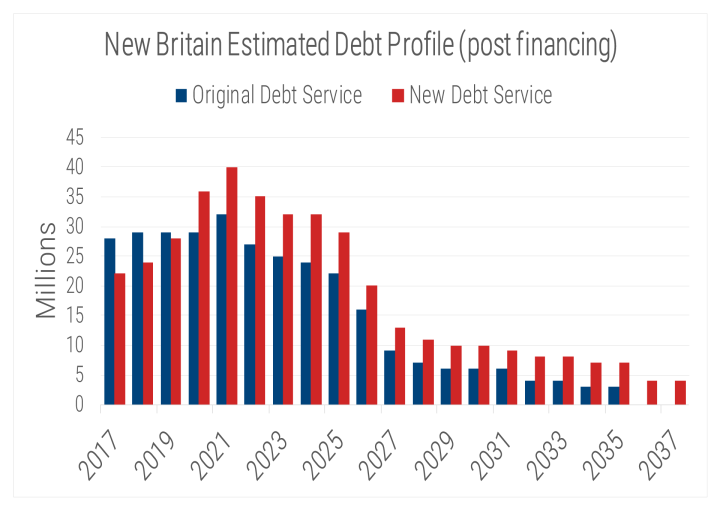

City and town officials, including Mayor Stewart, are correct that state government’s continuing fiscal problems can adversely impact local government finances. Moody’s Investor Services, however, did not cite state budget woes for New Britain’s latest downgrade in the municipal bond market. Instead the investors’ rating agency pointed to the city’s higher debt costs alluding to new deferments on short-term and capital bonding that will spike interest over the next five years or more. Whereas consumers and governments usually look to re-finance for lower interest rates the Stewart administration is doing the opposite, re-financing debt that will result in sharp interest rate increases in the near term.

Early this year the Stewart administration and the Common Council pushed the city’s debt further into the future after being told by bond counsel that interests rates would rise in the out years. The result was a short-term $6 million savings to be paid back with much higher interest after the current fiscal year ends.

Editor’s note: This column was originally published in NBPoliticus.